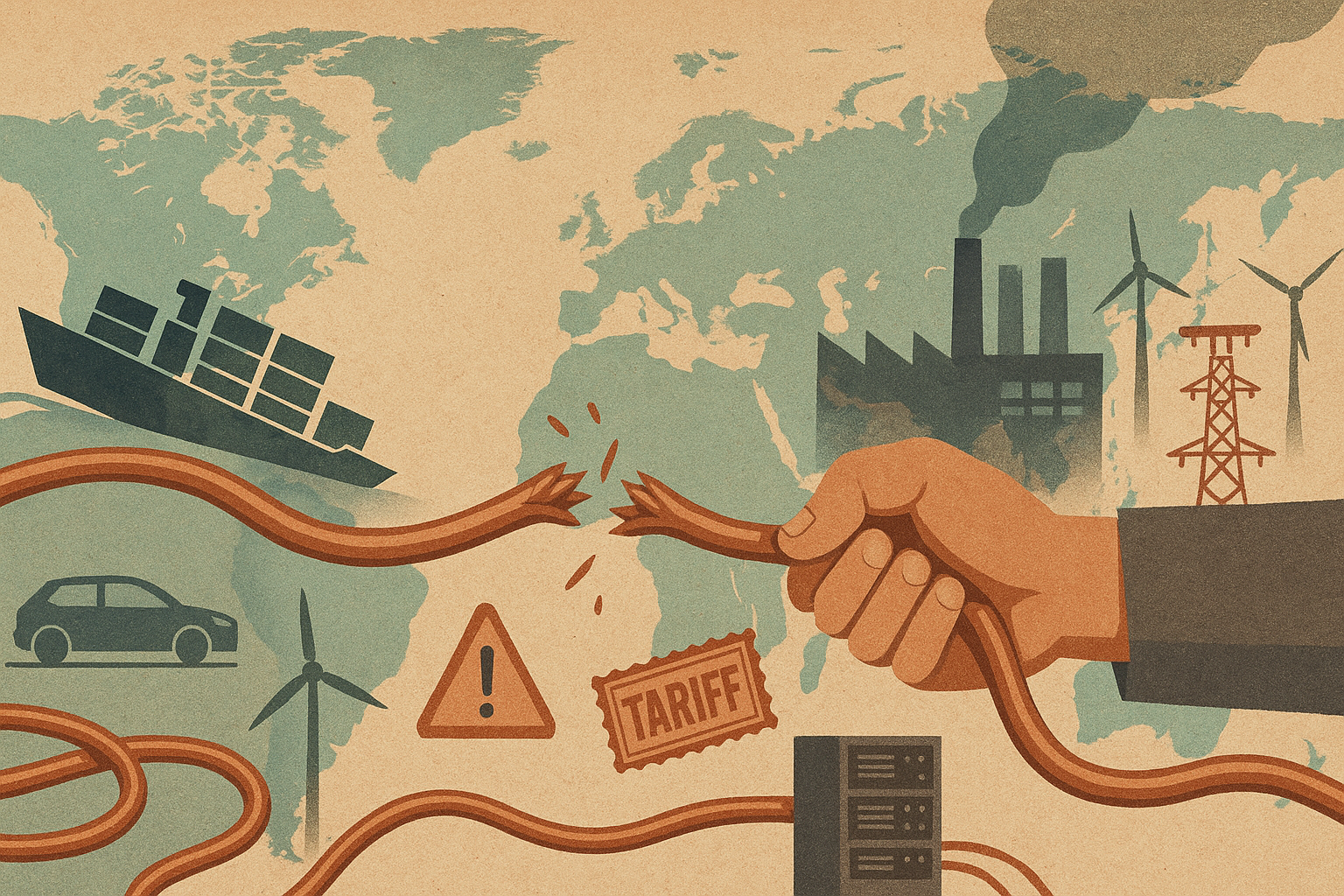

Copper is often dubbed “Doctor Copper” for its uncanny ability to take the pulse of the global economy. It is a critical input in a swath of industries driving the 21st-century transition: electric vehicles (EVs), renewable energy grids, AI infrastructure, and defense technologies.

An EV requires three to five times more copper than a comparable gasoline car—roughly 90 kg in a battery-electric sedan versus 18 kg in a conventional model. Each onshore wind turbine uses approximately 3–5 tons of copper, while offshore turbines demand even more. Solar power installations and energy storage systems rely on roughly 5.5 tons of copper wiring per MW of capacity. In data centers and AI infrastructure, copper is indispensable for high-voltage cabling, semiconductors, and thermal regulation. Even military hardware depends heavily on copper—used in ammunition, vehicles, radar, and electronics—meaning conflicts such as the war in Ukraine have unexpectedly fueled additional demand.

In short, copper has become the metallic backbone of electrification, digitization, and defense. Its importance has escalated from industrial necessity to strategic resource—“the mineral most fundamental to the human future,” as one study aptly noted.

Shifting Trade Flows and Global Supply Strains

Even before tariffs shook the market, copper supply chains were under strain. Over 50% of global copper reserves are concentrated in five nations: Chile, Australia, Peru, the Democratic Republic of Congo (DRC), and Russia. New mines take 15–25 years to develop, and ore grades are declining.

China dominates global copper trade, importing 60% of the world’s copper ore and producing over 45% of refined output. Its smelting dominance stems from decades of industrial investment. Asia’s share of global refining has tripled over the past three decades. In contrast, the U.S. and Europe rely on imports.

The U.S. consumed ~1.65 million tons of refined copper in 2024 but mined only ~850,000 tons—leaving about 45% of its needs to be met externally. The EU sources concentrate and cathodes from Chile, Peru, sub-Saharan Africa, and beyond. Major smelters like Aurubis in Germany warn that Europe remains vulnerable to disruptions.

China’s demand continues to surge. In early 2025, its copper concentrate imports hit record highs—up ~24% YoY in April—driven by new smelter commissioning. Simultaneously, Beijing expanded its strategic reserves of copper, cobalt, nickel, and lithium, reinforcing its long-term resource security doctrine.

The U.S., lacking similar leverage, has invoked the Defense Production Act, pursued domestic mining, and floated resource-for-security deals (such as access to the DRC’s copper-cobalt reserves). Still, processing bottlenecks persist: global smelters are short on concentrate, pushing treatment charges to record lows—sometimes even negative. This structural tightness made markets especially vulnerable to policy shocks.

Tariffs and Trade War Turbulence

In early 2025, geopolitics triggered a shockwave through the copper market. The catalyst: the Trump administration’s aggressive trade posture. In February, the White House launched a Section 232 “national security” investigation into copper imports—foreshadowing potential tariffs akin to those levied on steel and aluminum.

Though no copper tariffs were finalized at the time, the market responded swiftly. By mid-February, U.S. copper futures on COMEX surged over $1,000 per metric ton above the London Metal Exchange (LME) price—a massive arbitrage, suggesting traders were pricing in a 10–15% tariff.

China quickly retaliated. In April, following sweeping U.S. tariffs on Chinese goods (reportedly raising average duties to 54%), Beijing imposed export controls on seven heavy rare earth elements, including dysprosium, terbium, and scandium—vital for electric motors and defense applications. The restrictions applied globally, not just to the U.S., throwing entire supply chains into disarray. China also hit U.S. goods with a 34% retaliatory tariff.

Although copper wasn’t directly targeted—China is a net copper importer—Beijing’s message was unmistakable: it would weaponize critical minerals to defend its interests. China also accelerated copper stockpiling for its state reserves, signaling a strategic hedge against future supply disruptions.

Meanwhile, the U.S. moved cautiously. In early April, base metals (including copper) were exempted from immediate retaliatory tariffs. Analysts saw this as an effort to shield domestic manufacturing from collateral damage. Still, officials made it clear that copper tariffs could follow quickly once the Section 232 study concluded.

Market anxiety intensified. As Reuters’ Andy Home noted, “no one knows which way Trump’s tariff roulette wheel will spin next”—and that uncertainty alone was enough to roil business confidence across the copper ecosystem.

Record Price Gaps and Regional Distortions

By late March 2025, the price dislocation became historic. U.S. COMEX copper surged to $5.277/lb (≈$11,630/ton)—an all-time high—while LME copper lagged at ~$10,100/t. The arbitrage gap of over $1,600/t was unprecedented, reflecting panic-buying and tariff bets.

This created an arbitrage frenzy. Traders bought copper in Asia and Europe at LME-based prices and shipped it to the U.S. to capture the massive premium. Mercuria estimated that up to 500,000 tons of copper—about 2.5% of global demand—was diverted toward American ports.

The fallout:

• U.S. COMEX inventories doubled in weeks, surpassing 108,000 metric tons—the highest since 2018.

• LME on-warrant stocks plunged to just 116,000 tons globally by mid-April.

• Europe saw cathode premiums surge to $250/t in Germany, with processors calling the market “severely short.”

• Scrap copper prices in Europe approached parity with refined copper—an unusual, extreme signal of physical tightness.

Even China felt the ripple. Chinese smelters began exporting refined copper for profit, driving domestic inventories down. The Yangshan import premium jumped from $35 to $87/t, signaling renewed demand for incoming metal.

Volatility became the norm. When the White House hinted at a copper tariff delay in early April, the arbitrage collapsed from $1,600 to $230/t—only to rebound above $1,000 days later when new tariff signals emerged. The yo-yo effect left traders scrambling and producers anxious.

Stockpiling and Resource Nationalism

The 2025 copper crunch isn’t just a product of tariffs—it’s the result of deepening resource nationalism and strategic stockpiling across multiple continents. China leads the charge. Alongside its April rare earth export controls, Beijing ramped up strategic stockpiles of copper, cobalt, nickel, and lithium. Its State Reserve Bureau (SRB), known for counter-cyclical metal purchases, began accumulating copper during price dips. This aligns with Xi Jinping’s broader self-reliance agenda and BRICS-wide efforts to reduce exposure to Western-dominated supply chains.

BRICS nations and resource holders are following suit.

• Chile, the world’s top copper producer, has introduced higher royalties on large copper mines to fund social programs.

• Peru, ranked second globally, faces intermittent output disruptions from political unrest and community blockades.

• DR Congo, a rising player, continues renegotiating contracts—particularly with China—seeking better terms and local benefit-sharing.

While these moves don’t constitute direct export bans, they introduce volatility and redirect flow—often toward China through strategic bilateral agreements.

Indonesia, however, has been more explicit. It banned nickel ore exports in 2020 and intended to ban copper concentrate exports by January 2025 to force local smelter investment. Although a temporary six-month permit was granted due to project delays, the long-term trend remains clear: forcing upstream players to refine in-country, thereby tightening global supply.

Meanwhile, the West is responding with parallel strategies:

• The EU’s Critical Raw Materials Act includes copper on its strategic list and emphasizes supplier diversification and recycling.

• NATO and the U.S. Department of Defense have begun reevaluating copper as a defense-critical input. Proposals are on the table to expand strategic reserves.

• The U.S. has considered including copper in the National Defense Stockpile and is pushing legislation to incentivize copper recycling, which already supplies ~20% of the global market.

A subtler form of stockpiling is also underway via infrastructure deployment.

• China’s 2023–24 stimulus poured capital into power grid upgrades and rail networks—both copper-heavy sectors.

• In the West, legislation like the U.S. Inflation Reduction Act and EU Green Deal is translating into large-scale copper consumption through EV chargers, grid modernizations, and renewables—effectively locking copper into place for decades.

Once installed in motors, cables, or transformers, copper is effectively “out of circulation” until product end-of-life. As a result, available copper is not only scarce—it’s increasingly illiquid.

Impacts on Manufacturing and the Energy Transition

The copper dislocations of 2025 are rippling through manufacturing, energy, and defense sectors—each highly dependent on stable, affordable copper supply.

In the U.S., manufacturers are feeling the tariff premium directly. Wire and cable producers have seen input costs surge in tandem with COMEX copper prices. This cost pressure feeds through to a broad array of downstream products—electrical panels, consumer appliances, industrial equipment—raising inflationary risks.

In Europe, the problem is less about cost and more about access. With copper flows diverted toward the U.S., European buyers face delivery delays and have resorted to sourcing scrap. By April, copper scrap in Europe was trading at nearly 98–99% of LME value—historically high, and a clear indicator of supply scarcity.

For automakers, especially EV manufacturers, the disruption is more acute. Each electric vehicle contains 80–100 kg of copper across its motor, battery wiring, inverter, and charging system. A sustained price premium or shortage raises production costs, squeezes margins, and could delay rollout schedules.

The threat is particularly serious for North American supply chains, which rely on cross-border integration. For example, the U.S. exports copper wire to Mexico for harness production, which is then re-imported for final assembly. Tariffs on intermediate copper goods risk undermining this supply loop, potentially pushing manufacturers to offshore even more production to Asia—contrary to the nearshoring trend of recent years.

Renewable energy developers are also on alert.

• A 100-MW wind farm can require up to 300 tons of copper for turbines, transformers, and grid connections.

• Solar installations consume 5–6 tons of copper per MW.

Rising costs threaten to derail project timelines and budgets—at a time when governments are racing to meet 2030 emissions targets.

Some firms are evaluating aluminum as a substitute, particularly in power cabling. While cheaper and more abundant, aluminum has lower conductivity and performance limits—making it unsuitable for many high-tech or space-constrained applications.

The military sector is not immune. Copper is essential for ammunition, communications systems, radar, and armored vehicles. Defense planners are increasingly discussing the inclusion of copper in wartime stockpiles, especially as tensions with China and Russia escalate.

Finally, on the macro level, copper’s surge feeds into inflation indices. Producer price inflation, particularly in construction and electrical equipment, has ticked higher since March. Central banks are now monitoring copper as a proxy not just for industrial health—but for embedded inflationary pressure.

Historical Parallels and Outlook

The May 12, 2025, announcement of a 90-day tariff reduction agreement between the United States and China marks a significant, albeit temporary, de-escalation in their ongoing trade tensions. Under this accord, the U.S. agreed to lower tariffs on Chinese goods from 145% to 30%, while China reduced its tariffs on U.S. goods from 125% to 10%.

This truce has provided immediate relief to global markets, with stock indices rebounding and investor confidence improving. In the copper market, the easing of tariffs has led to a stabilization of prices and a reduction in the arbitrage-driven distortions that had previously disrupted supply chains.

However, this agreement is temporary and does not address the underlying structural issues that have contributed to the volatility in the copper market. Challenges such as declining ore grades, long lead times for new mining projects, and geopolitical uncertainties continue to pose risks. Moreover, the agreement excludes certain sectors, including automobiles, steel, and aluminum, which remain subject to existing tariffs.

As the 90-day period progresses, stakeholders in the copper market should monitor developments closely. The potential for renewed tensions remains, and the outcomes of ongoing negotiations will be critical in determining the long-term stability of the market. Strategic stockpiling, diversification of supply sources, and investment in recycling and alternative materials may become increasingly important strategies to mitigate future disruptions.

In essence, while the current truce offers a momentary respite, the copper market remains susceptible to the broader dynamics of international trade and geopolitical relations. As history has shown, copper is not just a metal—it is a message.

Leave a Reply